COVID-19 sheds light on the lack of communal health and economic infrastructure and societal investment. The cost of inadequate systems and investment will be worsened by flawed economic policy. And the indirect damage the virus causes through economic ripple effects will be large as households strive to balance credit obligations.

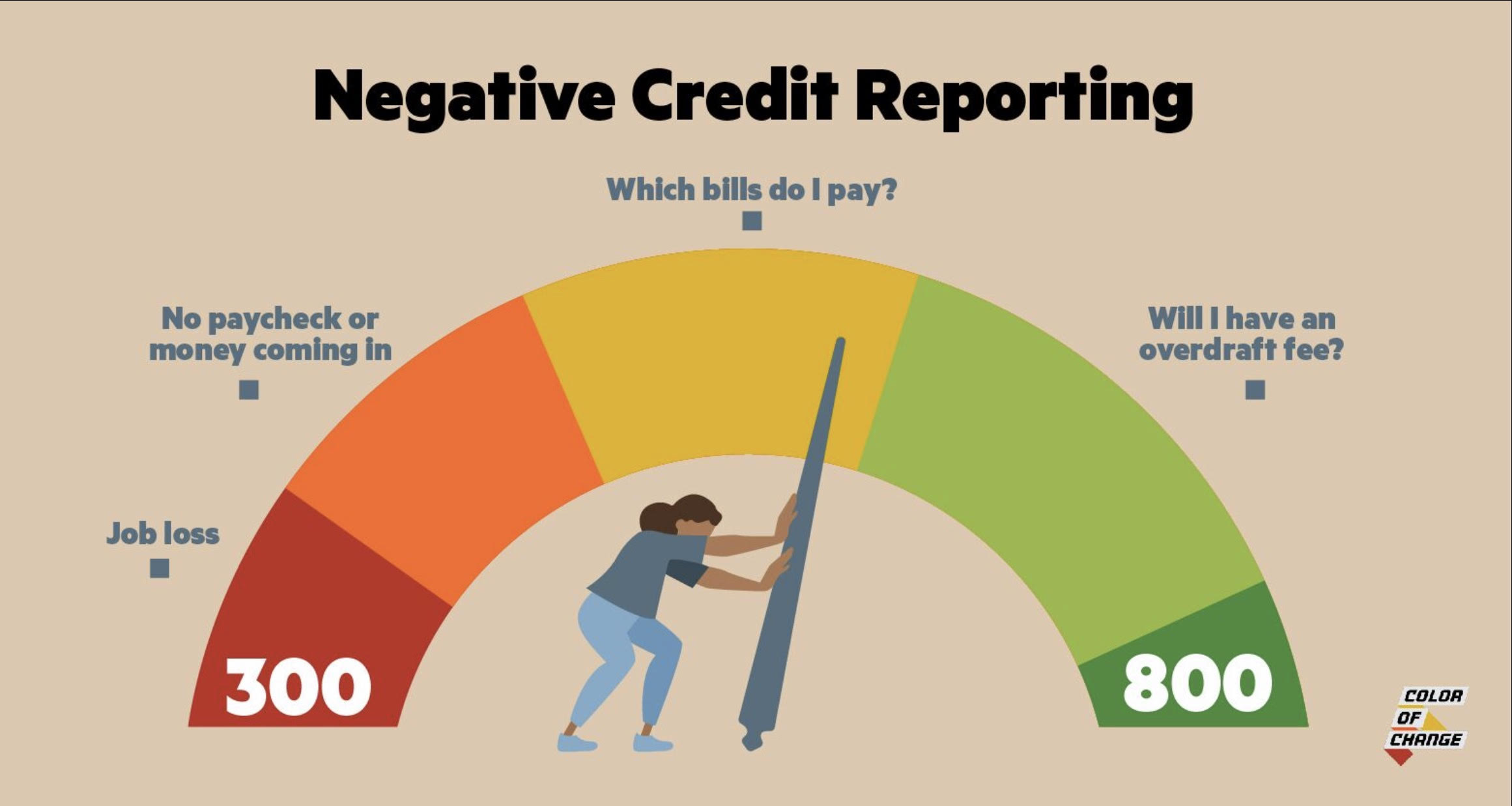

Individuals and families affected by this crisis should not be punished for any unexpected hardship resulting from this outbreak. With a directive to remain at home and practice physical distancing, many people face significant burdens of covering living expenses, including housing, groceries, and medicine. With so many households living paycheck to paycheck, the sudden nature of this pandemic has further interfered with people's ability to financially respond to the pandemic.

Credit inequality contributes to the racial wealth gap. Since the 2008 economic downturn, many Americans have had an easier time accessing credit. Restrictions have eased, and that has allowed millions to buy homes and start businesses. The recovery has worked well for Americans generally — except Black people. Black families have ten times less wealth than white families and credit is a byproduct of why. As the wealth gap continues to widen, suspending negative credit reporting during and after the Coronavirus pandemic, would help limit the financial harming Black families face.